Hair Trigger

- May 12

- 4 min read

DJT has some 'splaining to do. He got us into this mess, so he'd better hurry up and get us out of it. The market has been merrily heading toward new highs until today. I guess nobody believes he won't capitulate at some point, but when? Welcome to the orange hair-trigger world.

Recent market behaviour has given us a lesson in humility. The linkage between the front page and the business pages seems irreparably broken. As I wrote a few weeks ago, the S&P 500's elevated level suggests people are inclined to shrug off the War in Iran and its effect on the cost of living. The FOMO that began during the post-COVID bull market is still driving the bus. Earnings have been spectacular. The employment data last Friday showed no evidence of job losses due to the AI boom. Nobody cares that gasoline is $5/gallon when they are chasing the AI momentum trade.

And what a trade it's been! Samsung Electronics' stock has been the poster child of the recent rally in the chip sector. It is now 90% above its 200-day moving average, although it reversed today on talk of a new AI revenue tax in Korea. But the lack of volume confirmation for this recent rally is even more telling. Nobody is adding to their positions with fresh buying. A classic 5-wave exhaustion top is forming here.

Samsung Electronics

So, what else could signal a reversal of such widespread complacency? If only there were a sign.

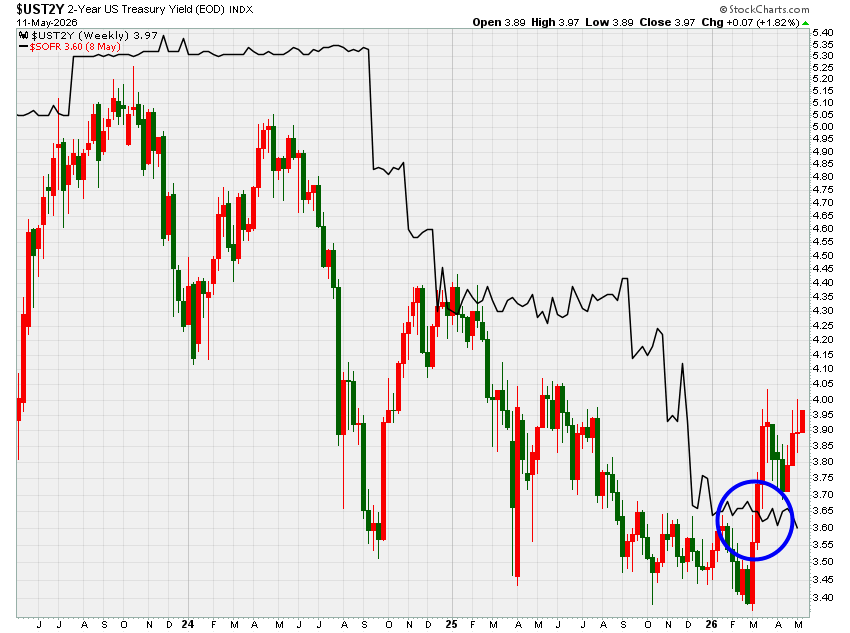

I think it's hidden in plain sight. The money markets have pulled a trigger on risk appetite, and nobody has noticed. Quietly, the cost of capital has started to rise. Two-year yields are now above overnight rates and are poised to rise further. The yield curve has started to bearishly steepen!

The chart below shows the 2-year versus SOFR - the Secured Overnight Financing Rate (shown in black). It's the money market facility directly managed by the Federal Reserve that indicates the Fed's desired level of interest rates. The 2-yr note is determined by market expectations. And those expectations are rising rapidly. The Fed is now firmly behind the curve.

U.S. 2 Year Yield vs SOFR

So, now that he has lost control of the market, what can Kevin Warsh possibly do to lower rates? The market has given up on Trump's sock puppet Fed Chair already! Today's 10-year auction had better go well, or a 5-handle may spook the bulls further. I'm watching the 3-month T-Bill closely here - anything above 4% would constitute an outright sell signal for risk assets.

And the CPI print this morning confirmed inflationary pressures are seeping into the U.S. economy. Although headline inflation was above 4%, core CPI is still below 3.0%. But the pass-through of energy and food prices is still building into the numbers, which are higher than expected. The Federal Reserve likely won't hike, as Warsh & Co. will continue to look past these numbers. But any thoughts of "easing" anytime soon are wishful thinking. Hey, wasn't that one of the catalysts for the market rally earlier this year?

So how does the annual 'sell in May, and go away' play out this year after spectacularly failing to work last year? Your guess is as good as mine, but the AI momentum jockeys are whistling past the graveyard now that the money markets have turned against them. And a quick resolution to the Iran debacle looks doubtful, especially if the Trump-Xi summit goes sideways on Thursday as I expect.

I still recommend holding/building some dry powder despite the Index-level bullishness. The breadth and volume confirmation indicators are flashing a warning as the few remaining performance chasers ride the last of the positive seasonality.

Bulls make money, Bears make money, Pigs get slaughtered. If you are still playing this rally from here, I suggest you have a hair trigger on the button. Oh, and it's orange, too.

Risk Model: 5/5 - Risk On

With the RSI at 56 and the XIUs only 8% above their 200 moving average, you aren't getting any sell signals here. The AAII Sentiment is in a momentum-chasing recovery mode, and the 3-month VXV is surprisingly well contained despite the headline risks. The Model is likely to change on any negative headline, as both sentiment and implied volatility could reverse sharply. Again - the hair trigger environment at work!

Copper/Gold is interesting. Despite the global energy shock, supply-side effects are driving prices higher. Major mine expansions have been slow, and Chinese inventories have been dropping sharply. Although the ratio has definitely broken out, it is a bit extended. Given the recent history of head-fakes in this relationship, I'd like to see more work before I call a trend change - especially since copper seems to be the hard asset of choice for punters playing the AI bubble now that Bitcoin and Gold have corrected. Despite that hype, a seasonal high in copper is likely, especially given speculators' excessive positioning.

Copper/Gold

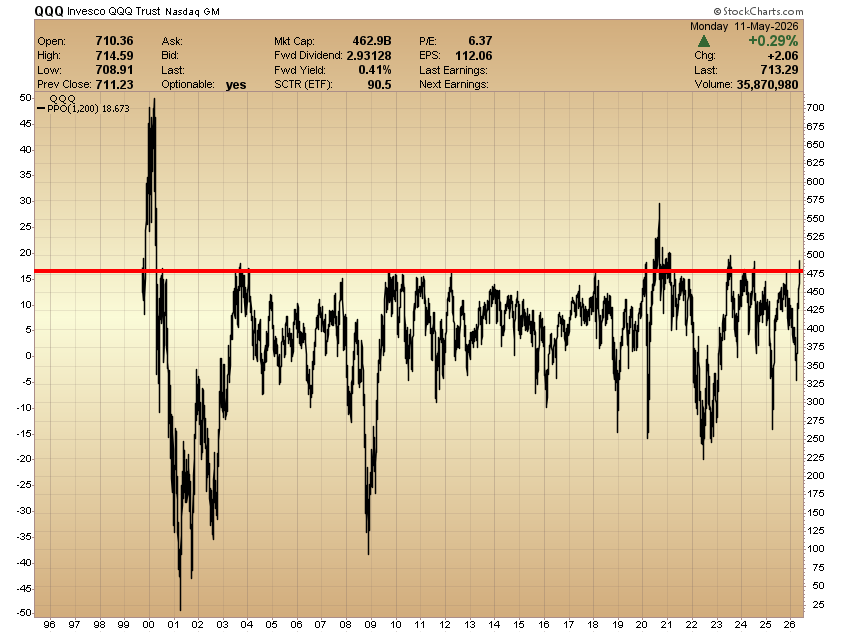

Looking at the Nasdaq ETF - QQQ - here at an extended level above its 200-day moving average. It's currently reading 18%, a level that rarely holds.

Although Dot-Com-era comparisons are popular, it remains well below that level of froth. Still, it won't stay here for long if this chart is any guide.

QQQ ETF

Comments