Stalemate

- May 5

- 4 min read

When two opposing forces have equal power, a stalemate occurs. That sums up risk markets today.

Investors find themselves torn between two conflicting motivations: continue playing the AI-driven bull market strength or sound the retreat amid rising rates and slowing economic growth. This dynamic has created a stalemate in investors' risk appetite, leading to a trading range market.

Earnings are rising at the fastest pace since the post-COVID recovery period. The price-earnings ratios that kept bearish investors out of this bull market are coming down quickly, offering comfort to the now-vindicated bulls. The interplay between surprisingly strong earnings and slowly rising interest rate expectations is keeping investors, on balance, cautiously optimistic. Scared to be caught offside, yet not confident enough to go 'all in' on risk-taking.

But when three companies, Alphabet, Meta, and Amazon, account for 70% of the increase in S&P 500 earnings, caution should be the byword. And has anyone noticed the rally in the 2-yr bond yields? I thought the Fed's rate-cutting cycle was one of the primary drivers of the rally since last year. Does anybody think this chart suggests rates are headed lower?

Adding to the angst is the thought of an unholy alliance now between the US Treasury and the Federal Reserve. Treasury boss Scott Bessant has agreed to allow the Fed to keep rate cuts on hold for now due to the Iran crisis. How long before the solution to the war is used by the newly appointed Fed Chair, Kevin Warsh, as an excuse to cut rates?

And make no mistake, the now closed Straits of Hormuz will reopen. The political pressure on the Trump administration for a TACO-style deal, even from his own party, is growing as the midterms approach. When oil starts flowing again, the stock and bond markets will rally. That has the potential for a last gasp blow-off top for the now long-in-the-tooth bull market.

The rally that I envision should help the left behind components of the market, more economically sensitive and non-AI related, participate. As I wrote last week,

"My strategy here would be to hold some dry powder for a further pull-back. The small backup in longer-term yields on higher-for-longer oil prices is also a convenient excuse for the profit-taking. The spectre of a stagflationary oil shock will crimp Industrial stocks as well. But I'm getting ready to buy them on any weakness."

I still hold to this view, and despite the stubbornness of the earnings-driven rally, I believe a further short-term pullback is warranted, especially as the 2-yr yields back up and oil continues to elevate.

Ultimately, the oil market holds the key. Should the futures market price in a sharp decline in crude oil costs as a result of a peace agreement, the ensuing rally will reflect all the good news of a robust economy and an easy Fed. The 'sound of trumpets' will be heard. But that's when you start to worry: what could go wrong?

In a word: bonds.

Look below for the indicators of a stressed-out bond market. It's more about supply and demand than sentiment or inflation premium. The lack of fiscal prudence in Washington is being masked by the headlines from Iran. Even before the costs of "Epic Fury "were calculated, the U.S. Treasury was set to issue a rising amount of short-term notes this year. And how much longer can they rely on shortening the issuance term structure? At some point, they will have to start ramping up the 10-year again. A 5-handle-long bond won't go over well with Wall Street and its pricey stock market. Higher term premiums are here to stay.

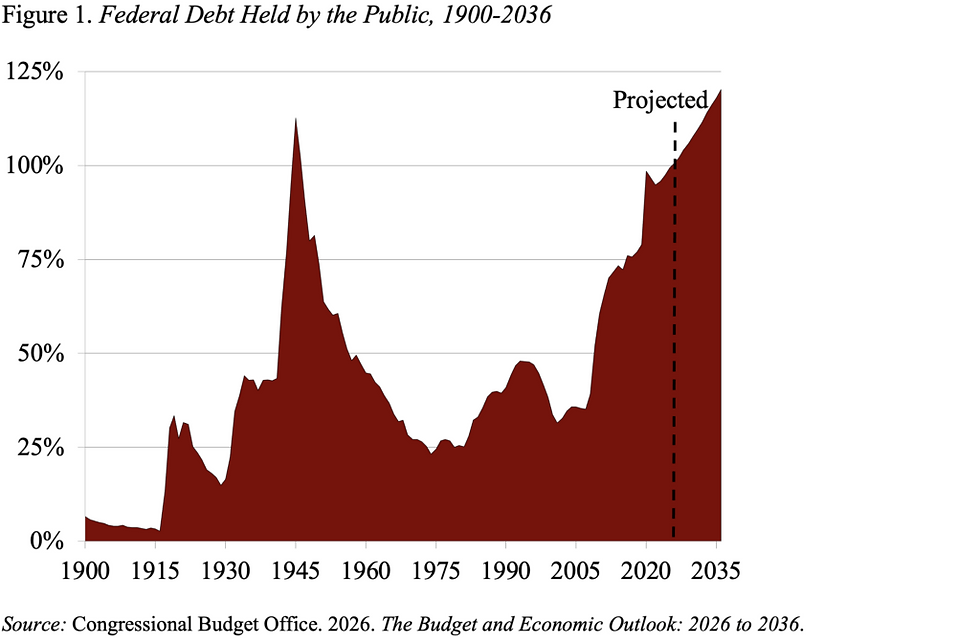

The sheer amount of debt embedded in the system is projected to surpass that of the WW2 era shortly.

And the debt service costs are rising rapidly, accounting for an ever-increasing percentage of the economy.

So how do Bessant and Warsh stickhandle the next six months? The political climate is unwelcoming to any sense of fiscal discipline - and that's before you factor in Trump's quixotic quest for low rates. Who in their right mind would dare to turn off the spending tap now with an election staring them in the face?

For now, don't worry, be happy. Any thoughts of a stagflationary stalling out should soon be put to bed as the oil shock eventually dissipates. We've seen this game being played out in the Middle East before, and it always ends the same way. I'm betting that oil prices will collapse later this year. That will be the end of the good news, though. Stalemate over.

Risk Model: 4/5 - Risk On

Although notionally bullish, the model missed the rally and is trying to play catch-up. Sentiment has fallen back this week, as investor caution creeps back into the picture. The hallmark of the post-COVID era has been the strength of FOMO. You see it whenever the market responds well to even the hint of good news, such as this morning's reaction to events in the Gulf. It's been a tough tape to fight for anyone with a bearish bent. The bears will have their day at some point, but for now, it's risk-on.

Comments