Get Real

- Jun 16

- 5 min read

Now that the SpaceX IPO has cleared the launch pad and is headed towards Mars, the market can go back to chasing its tail. Or should I say tale - like the one that brokers are telling clients. Can they continue to entice clients to pile into the AI momentum trade? Or should they diversify their risk in a market that continues to focus on a single theme?

The FOMO induced rally is running on fumes as the surge in supply - IPOs and debt issuance - is matching the incremental demand for AI exposure. And just as questions are beginning to arise about the efficacy of agenic apps at the customer level. A recent MIT study found that 95% of generative AI pilots failed to deliver measurable productivity gains, and corporate CEOs are increasingly questioning AI spending. Nosebleed valuations aside, investor fatigue is weighing on sentiment. The breadth of the AI market is diminishing, as fewer stocks are reaching new highs in the highly concentrated NASDAQ100, even though the index itself has reached a new peak. This, dear reader, is how tops form.

NASDAQ New Highs

So with the risks of the AI boom turning into a self-fulfilling bust - or at least pausing for breath - where can investors hide?

I think it's time to get real - as in real assets. For the past 28 years, since the GFC, we have been in an era of easy money. With the huge surge in money creation through ZIRP, QE, and record debt-to-GDP levels, there is too much money chasing too few goods. So far, the goods that investors have been chasing are stocks. How long before that starts to translate into excess demand for more tangible assets? I don't know, but that is always the ultimate destination for liquidity as the economic cycle extends into its inflationary latter stages.

The Fed's laissez-faire policies should continue now that a fox is in the henhouse. The installation of Trump's hand-picked minion, Kevin Warsh, as chair of the Federal Reserve should worry anyone who fears currency debasement. Although he talks a good game about defending against inflation, his real test will come later this year, when the post-Iran supply shock wears off, and inflation rises anew. Next week should see a bit of rope-a-dope on the part of the new Chairman, as he faces the risk of angering both the bond market and/or DJT if he makes a bold step in either direction. By cutting back on Fed communication, as he has stated, he will attempt to lay low for now.

So, in the latter half of the Roaring '20s, we increasingly find ourselves in an inflationary world. The inexorable rush to perpetuate a full employment economy is mostly to blame. Why else does the Fed maintain an official 'easing bias' and a quixotic desire for 2% inflation when that goal hasn't been reached during the post Covid era? It seems the sooner the Fed admits 3 is the new 2, the better. Price tags don't vote; people with jobs do.

CPI

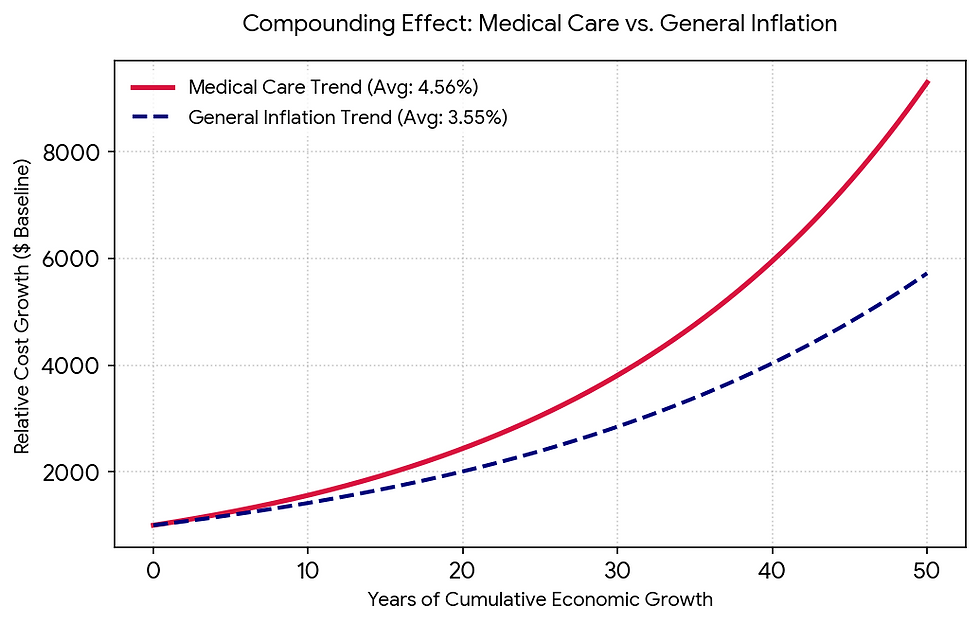

Yes, the AI boom is a deflationary force as labour productivity should increase, thus lowering unit costs. But if you think that demographics will bail us out, think again. The most persistent inflationary force over the past 50 years has been Medical Care. That trend can only accelerate as the inevitable Boomer age-outs drive demand for health care higher. The weighting in the CPI basket may shift from iPhones to IVs.

Medical Care Inflation

So what is the best entry point for this rebalance? I was taught long ago to avoid the impulse to run with the herd for too long. As my first boss at Prudential Insurance, Martin Anstee often warned me, "Don't shoot where the rabbit was". Remember, they don't ring a bell at the top (or bottom), so it is time to do some bottom fishing.

Commodities and other 'hard' assets, to most people, are anachronistic relics of a time gone by. Although they once dominated the wealth creation of entire economies, those days are long gone. I'm not arguing for a wholesale dumping of all winning trades, but there are signs of a bottoming out in the various hard asset categories that are readily available to receive some love now.

Below are the relative performance charts for various commodity and stock indices compared to the TSX ETF.

Gold

Last year was a stellar year for gold as an investment, supplanting Bitcoin as the alternative to fiat currencies worldwide. I think of gold as the gateway drug for hard asset investors. This pullback should start to base shortly, but the longer-term seems to be marked by higher highs with each rally. Bullish.

Oil

The performance of energy stocks has awoken from its slumber due to the sudden realization that, despite various greenification efforts, it is, in fact, a necessary evil for economic performance.

Base Metals

Given new life by the AI electrification boom, base metals are breaking out against the broad market. Bricks and mortar aren't just for housing anymore, as copper demand from the grid buildout has consistently outpaced supply additions.

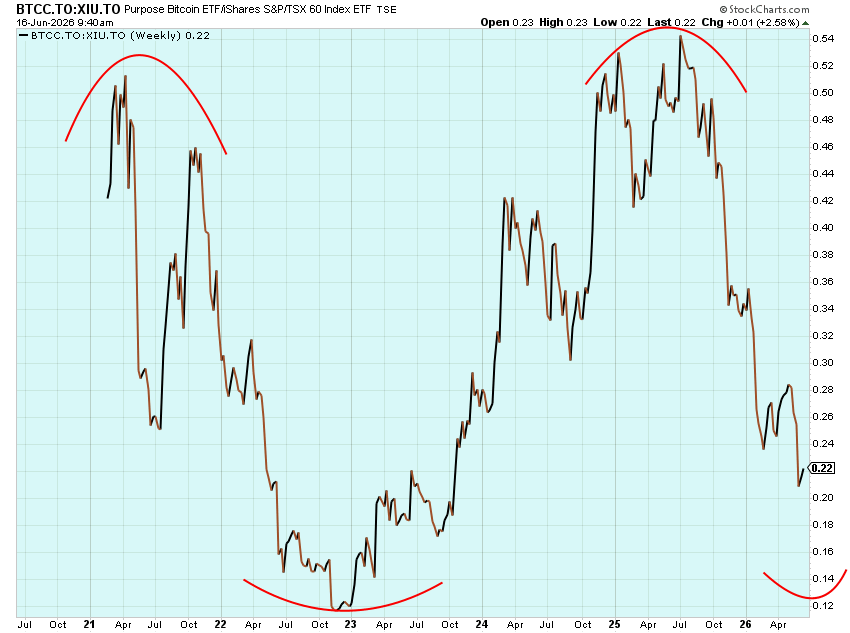

Bitcoin

The Crypto winter is blowing a cold wind on the neck of this once heralded asset. But isn't the role of a hard asset to diversify the risk by being uncorrelated to your other holdings? With the RobinHoodster early adopters now out of the way, it might be worth another look at this ersatz 'hard' asset class. The pattern that is emerging is intriguing, don't you think?

Real Estate

After its existential crisis in 2008 and a brief, but doomed, resurrection in 2012, real estate has become like a sinking stone in investor portfolios. Commercial real estate has suffered from demand destruction across all sectors due to the e-commerce and work-from-home trends. But they're still not making any more of it - especially now that the forest of cranes in Toronto and most other major cities has been cut down. I suspect this may be the most contrarian play in the capital markets today. You have to like it for that fact alone.

I may be 'hard' for you to believe, but now might be a good time to get real.

Risk Model: 2/5 - Risk Off

This week carries the risk of a "Sound of Tumpets" rally reaching exhaustion. Previous momentum-led rallies were all-inclusive. This week, it really mattered whether you were in SpaceX or not, as the likes of Nvidia, Microsoft, and Netflix lagged badly, and Apple barely kept up. And that's before the next wave of selling to make room for Anthropic and OpenAI. They had better go well.

The Model is notionally bearish only because the AAII survey is pre-Iran MOU. The XIU main price variables - RSI and % Above 200DMA are becoming overbought, offering a note of caution. The VXV and Copper/Gold variables are saying all clear, but an exhausted tape is starting to wear on investors' bullishness. Bonds are feebly rallying off the oil dip, but it seems they still seem worried about something. Should anything go bump in the night as a result of the Fed news conference, watch out below.

Comments